For years, the $800 de minimis threshold supported the rapid expansion of eCommerce brands. This entry point allowed businesses to ship individual parcels directly to U.S. consumers without paying duties or filing formal paperwork. But that era has ended.

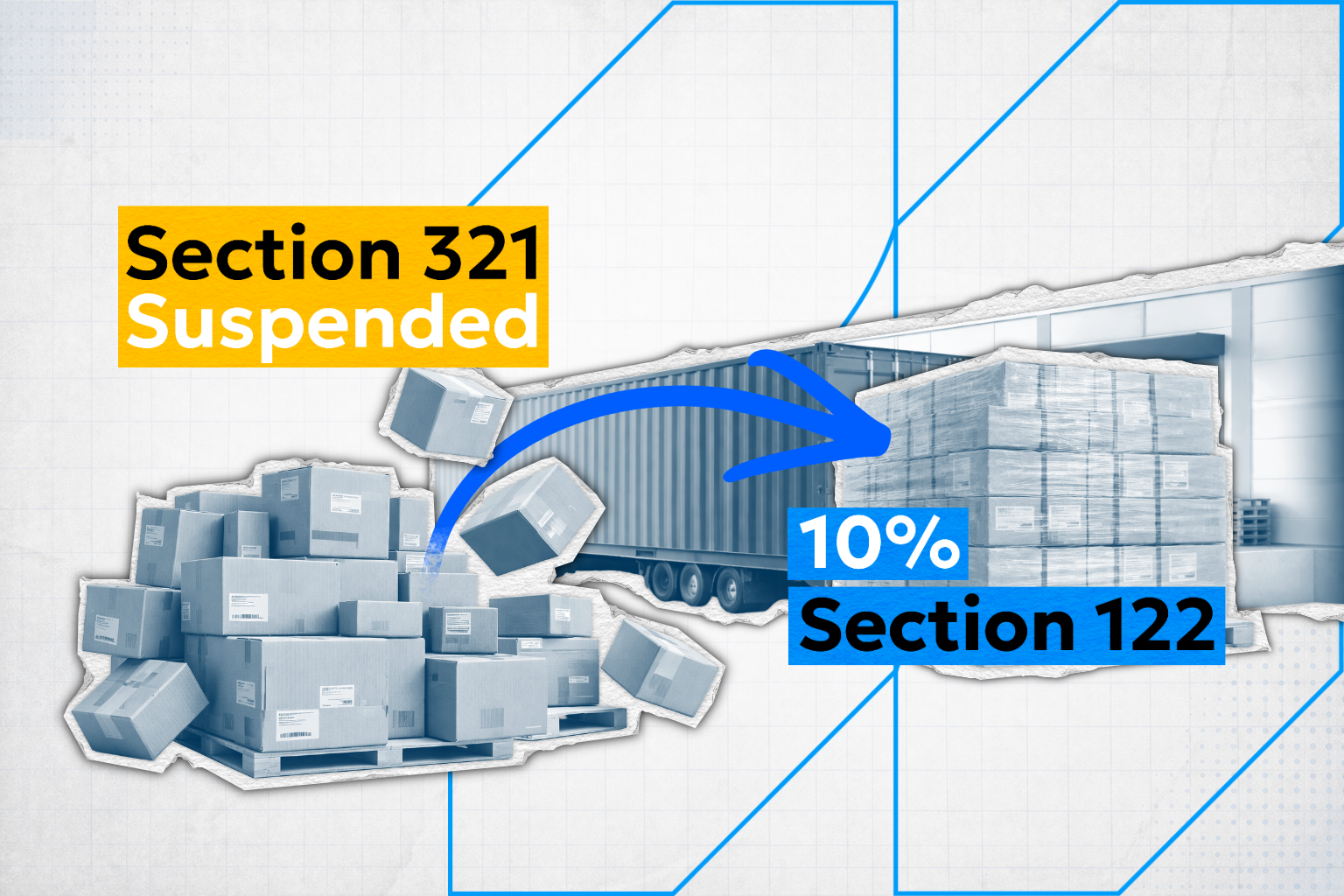

In February 2026, the U.S. government announced that the global suspension of Section 321 would remain in place for all trading partners, including China and Hong Kong. Operational success in 2026 hinges on finding a way to stay compliant with import regulations and maintain margins despite these new barriers. This article provides a roadmap for navigating the current environment, from calculating new Section 122 surcharges to implementing formal entry protocols.

Breaking Down Section 321 De Minimis

A series of rapid legislative and administrative actions over the last decade led to the current state of eCommerce imports. Understanding these regulatory milestones helps clarify why historical shipping strategies are no longer viable.

- 2016: The de minimis threshold increased from $200 to $800 under the Trade Facilitation and Trade Enforcement Act (TFTEA).

- May 2025: Customs and Border Protection (CBP) suspended de minimis eligibility for all imports originating in China and Hong Kong.

- August 2025: The One Big Beautiful Bill Act (OBBBA) cemented administrative suspensions and expanded them to include all global trading partners to prevent “country-hopping” by major eCommerce platforms.

- February 2026: The administration codified the permanent suspension of duty-free de minimis treatment and integrated the 10% Section 122 surcharge. This action followed a Supreme Court ruling that struck down previous tariffs based on the International Emergency Economic Powers Act (IEEPA). While the decision created temporary confusion regarding the legality of certain trade barriers, it did not reinstate Section 321 eligibility. Every country remains suspended from de minimis treatment today.

To summarize: low-value shipments no longer enter the U.S. duty-free. Importers must now file a formal or informal entry and pay all applicable duties immediately upon arrival. While the $800 threshold remains part of the federal statute, current administrative mandates prevent commercial eCommerce shipments from utilizing the exemption.

Calculating eCommerce Customs Clearance: Section 122 and New Tariff Costs

While the global surcharge represents a significant shift for eCommerce, it actually provides a more predictable baseline than the volatile IEEPA-based tariffs that dominated last year. During that period, retaliatory duties on China and Hong Kong imports fluctuated wildly, reaching as high as 125% at times. Section 122 replaced those unpredictable emergency tariffs with a standardized 10% surcharge, effective through July 24, 2026.

This change creates a double-edged sword for eCommerce brands. On one hand, the extreme tariff rates have dropped, offering relief to those who were hit hardest by IEEPA. On the other hand, the indefinite suspension of Section 321 de minimis means that the 10% rate is now inescapable. Even a $50 pair of shoes (which previously entered duty-free) is now subject to a $5 baseline duty plus administrative fees.

View the 10% rate as a temporary floor rather than a permanent ceiling. Ongoing Section 301 investigations into manufacturing overcapacity may lead to targeted duties that stack on top of existing rates later this summer.

Comparing Taxes, Tariffs, and Duties

Misunderstanding trade terminology often leads to significant errors in landed cost modeling. While these terms appear similar, they represent different financial obligations to the U.S. government.

A duty is a tax collected by CBP on an imported item based on value and HTS classification. A tariff is a specific duty used as a tool for trade policy to protect industries or rebalance trade deficits. Internal taxes, including the Merchandise Processing Fee (MPF) or Harbor Maintenance Fee (HMF), are administrative charges required to fund customs operations.

Life After De Minimis: What It Means for eCommerce Imports

The global suspension of de minimis eligibility changes the fundamental unit economics of cross-border eCommerce. The challenge isn’t about the 10% Section 122 duty, but the fixed cost of customs entry filings. Because customs brokers generally charge per entry – not per item – small, high-frequency shipments now carry a heavy administrative premium.

Scenario A: The Direct-to-Consumer Parcel Model

Consider a brand shipping 50 orders per day with a $50 average order value (AOV) directly from an overseas supplier.

- Old Model: $0 duties and $0 entry fees under Section 321.

- 2026 Model: A 10% Section 122 surcharge adds $5.00 in duties per order. However, the brokerage fee for an individual entry typically ranges from $25 to $75. For a $50 order, the total cost to clear customs can reach $80, effectively doubling the price of the product before it even reaches the last-mile carrier.

- The Strategy: Brands shipping lower volumes often consider domestic sourcing to eliminate import costs entirely. If international sourcing remains necessary, the only viable path is to halt individual parcel shipping and wait until order volume justifies a pallet-sized shipment for consolidation. While this adds 1-2 weeks to the delivery timeline, it prevents the business from losing money on every sale.

Scenario B: The Scaled Consolidation Model

A business shipping 500 orders per day faces the same per-parcel fees but has the volume to bypass them through faster bulk importing.

- The Strategy: Instead of 500 individual entries, you consolidate these orders into a single ocean or air freight shipment at the origin.

- The Value: You still pay the 10% Section 122 duty on the total commercial value, but you file only one customs entry for the entire lot. Paying a single $75 brokerage fee for 500 orders reduces the administrative cost to $0.15 per unit.

Checklist for eCommerce Freight Forwarding in 2026

The transition from de minimis to dutiable entries requires a rapid shift in how you manage supply chain data and vendor relationships. In today’s environment, a single classification error or a missing bond can trigger seized shipments and significant financial penalties. To stay ahead, consider taking the following steps.

- Re-classify and Re-calculate: Review every SKU in your library to ensure correct HTS codes are in place. Accurate classification is necessary to determine the specific taxes, duties, and tariffs that apply to your goods.

- Update Checkout Pricing: Adjust your checkout system to display estimated duties at checkout. You must decide whether to build these costs into the retail price or present them as a “landed cost” fee to avoid “duty-due” surprises for your customers.

- Secure a Continuous Customs Bond: Because you are now filing entries on all shipments, you should have a continuous bond on file with CBP. This bond acts as a financial guarantee that you will pay all required duties and taxes, enabling faster release of your shipments.

- Establish Brokerage Relationships: Partner with an experienced customs broker who understands high-volume eCommerce. You need a broker capable of handling the transition from Section 321 to formal or informal entry.

- Consolidate Shipments: Reduce your reliance on individual parcel shipping. Work with a freight forwarder to consolidate orders into larger ocean or air freight shipments to spread fixed entry costs across more units.

- Automate Compliance Data: Use digital tools to track landed costs and classification accuracy. Automation reduces the risk of human error during the entry process.

- Explore Alternative Sourcing: Evaluate suppliers in USMCA countries (Mexico/South America/Canada) or domestic partners. Reducing your reliance on high-tariff regions is the most direct way to maintain a competitive price point.

Meet Dedola: Your Dedicated eCommerce Freight Forwarder

Navigating life after de minimis, where every parcel is subject to duties, requires a partner who understands the freight consolidation and landed cost modeling. Since 1976, we have helped brands stay ahead of evolving trade policies by focusing on grounded, practical logistics. We provide the coordination and data visibility you need to manage Section 122 surcharges and formal entry requirements without losing your margins.

Download our Guide to Lower Duties for more tips, or schedule a consultation with us to take a closer look at your 2026 import strategy.

FAQs About Section 321 De Minimis

What happened to de minimis in 2026?

Executive Order 14324 solidified the permanent removal of Section 321 exemptions for all commercial eCommerce. This action reaffirmed the administrative suspensions that began in May 2025 for China and Hong Kong, which then expanded globally in August 2025 under the One Big Beautiful Bill Act (OBBBA).

While the $800 threshold technically remains in the federal statute (19 U.S.C. 1321), the Executive Order removes the “duty-free” status for commercial shipments, subjecting every parcel to current tariff regulations regardless of its low value.

How does the Section 321 suspension affect eCommerce brands?

The suspension eliminates the tax-free entry of parcels under $800, subjecting every import to the 10% Section 122 surcharge and any applicable category-specific tariffs.

Because these shipments no longer qualify for simplified de minimis processing, each parcel requires a 10-digit HTS classification and a specific entry filing. For brands using a direct-to-consumer model, the fixed cost of brokerage fees for individual parcels can now exceed the retail value of the product itself, making per-parcel shipping from overseas factories financially unsustainable.

What are the formal entry requirements for eCommerce imports in the USA?

Commercial shipments valued over $2,500, or those containing goods under the oversight of Partner Government Agencies (PGAs) like the FDA or EPA, require a Formal Entry (Type 01). Formal entries require a continuous or single-transaction customs bond and a 10-digit HTS code.

For eCommerce parcels valued under $2,500, importers typically utilize an Informal Entry (Type 11). While informal entries use a simplified process that generally does not require a customs bond, it still requires accurate classification and the immediate payment of all Section 122 surcharges and duties.